Qualcomm Sends Letter to Stockholders and Files Investor Presentation

Urges Stockholders to Reject Broadcom’s Dramatically Undervalued Takeover Proposal by Voting “FOR” Re-Election of Qualcomm’s Highly Qualified Board on WHITE Proxy Card

Qualcomm Executives to Give Video Presentation at 9:00 am ET, available at www.qcomvalue.com/investor-presentation

Qualcomm Incorporated (NASDAQ: QCOM) today sent a letter to its stockholders in connection with the Company’s 2018 Annual Meeting of Stockholders, which will be held on March 6, 2018. Stockholders of record on January 8, 2018 will be entitled to vote at the meeting.

In addition, Chief Executive Officer Steve Mollenkopf, Executive Chairman and Chairman of the Board Dr. Paul E. Jacobs, President Cristiano Amon, Chief Financial Officer George Davis and General Counsel Don Rosenberg will discuss Qualcomm’s clear path to significant near-term value creation for stockholders in a video presentation starting at 9:00 am ET available at www.qcomvalue.com/investor-presentation. At that time, Qualcomm will file an investor presentation with the Securities and Exchange Commission (“SEC”) and post it to www.qcomvalue.com/investor-presentation. The Company will also post a video featuring Mr. Mollenkopf discussing Qualcomm’s leadership position in 5G and the significant value creation opportunities ahead for Qualcomm stemming from its investments in 5G.

The stockholder letter, presentation and videos (and/or video transcripts), along with other materials related to the Company’s 2018 Annual Meeting, will be available at www.qcomvalue.com and at www.sec.gov. The website will be updated as additional information becomes available.

The full text of the letter follows:

![]()

January 16, 2018

Dear Qualcomm Stockholder,

For over 30 years, Qualcomm has pioneered the foundational technologies that have revolutionized how people connect and communicate with each other and the world around them. Our success in leading each new transition in mobile technology is the result of our intense focus on always looking forward – developing transformative technologies, establishing ecosystems where our products thrive, and driving sustainable value creation.

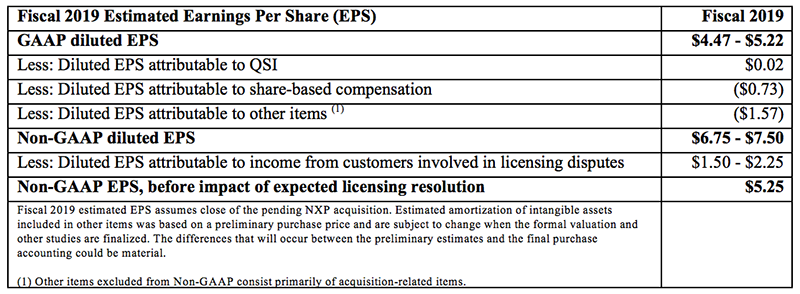

Today we are executing a strategy that we are confident will continue to generate significant value for our stockholders in the near term with additional upside. We are firmly committed to delivering $6.75 - $7.50 in fiscal 2019 Non-GAAP earnings per share (“EPS”). Our path to delivering substantial value to Qualcomm stockholders includes the continued strong performance of QCT, a cost reduction program that is specific and actionable, value creation from our NXP acquisition (or, alternatively, a large share repurchase) and the expected value upside from resolution of current licensing disputes. Moreover, our stockholders are also poised to realize the value of Qualcomm’s leadership position in 5G, which is in the early stages of transforming multiple industries, including mobile, IoT, automotive and many others. This is why we have rejected Broadcom’s attempt to acquire Qualcomm at an opportunistic and extremely low price, with a highly uncertain – perhaps impossible – regulatory path to completion.

Broadcom is asking Qualcomm stockholders to voluntarily transfer to a hostile acquirer the considerable near- and long-term value creation Qualcomm has in front of it. It is attempting to acquire Qualcomm at an opportunistic, inferior price by installing a slate of conflicted Broadcom/Silver Lake nominees with minimal relevant experience.

The Qualcomm Board strongly objects to Broadcom’s aggressive tactics and urges you to reject its solicitation efforts by voting FOR the re-election of Qualcomm’s highly qualified slate of directors on the enclosed WHITE proxy card today. Vote only the WHITE proxy card – please discard any Blue proxy cards you receive from Broadcom.

Your Board rejected Broadcom’s proposal because:

- It dramatically undervalues Qualcomm and does not reflect our clear path to near term value. Based on our committed $6.75-$7.50 in fiscal 2019 Non-GAAP EPS, the Broadcom proposal implies a P/E multiple substantially below peer trading multiples and precedent transaction multiples.

- It carries significant regulatory uncertainty – as the largest potential transaction in the technology industry, regulatory approvals could take 18 months or more and may require complex divestitures or operating restrictions making clearance difficult, if not impossible, to obtain. Divestitures will likely be demanded that may not be feasible in the face of national security and other issues.

- It gives no value to the transformative opportunity in 5G and Qualcomm’s ability, through its leadership position and targeted investments, to deliver significant stockholder value as we capture this opportunity.

- It asks stockholders to place a conflicted Board slate in place for a transaction that would likely not be completed for at least 18 months, if ever – exposing the Company to significant oversight risk relative to Qualcomm’s experienced and capable Board, as well as business risk during pendency of regulatory review.

- It is designed to benefit only Broadcom stockholders – not Qualcomm stockholders.

We urge you to block Broadcom’s attempt to capture, for itself, the value that rightly belongs to you as a Qualcomm stockholder, by voting FOR Qualcomm’s director nominees on the WHITE proxy card TODAY. Vote only the WHITE proxy card – please discard any Blue proxy cards you receive from Broadcom.

QUALCOMM HAS SIGNIFICANT BUSINESS MOMENTUM AND THE RIGHT STRATEGY TO CREATE BOTH NEAR-TERM AND LONG-TERM STOCKHOLDER VALUE – FAR GREATER VALUE THAN BROADCOM’S DRAMATICALLY UNDERVALUED PROPOSAL

Broadcom’s proposal is highly opportunistic and dramatically undervalues your Company’s leading market position and value creation opportunities.

Qualcomm Has a Clear Path to Creating Significant Near-Term Value

We have a specific game plan and are committed to delivering $6.75 - $7.50 in Non-GAAP EPS by FY 2019 through:

- Continued growth in our core business, driven by our recent wins

- A new $1 billion cost reduction program

- Accretion from our NXP acquisition (or, alternatively, a large share repurchase)

- Resolution of current licensing disputes

As is widely known, we are currently in litigation with Apple. What many stockholders do not realize is that we have binding long-term license agreements with Apple’s contract manufacturers. But Apple has required its contract manufacturers to cease paying us despite these existing binding contracts. Apple now continues to utilize Qualcomm’s intellectual property for its own profit without paying. In this litigation, Apple is seeking to avoid paying fair value for Qualcomm’s intellectual property, rejecting terms that are well established in the industry. Apple has often used such litigation to try to renegotiate with its suppliers, and Qualcomm has taken legal action to enforce our contracts.

While the legal process takes time, we believe we will successfully defend our licensing programs, as we have done in the past.

Qualcomm Stockholders Are About to Benefit from One of the Most Significant Technology Shifts and Market Opportunities in the History of Wireless: 5G

Broadcom’s proposal dramatically undervalues Qualcomm’s current business. Perhaps as importantly, it gives no value to the transformative 5G value creation opportunity that should play out as 5G is launched globally in 2019 – to the near- and long-term benefit of Qualcomm stockholders. As the driving force behind the next technological revolution, 5G will leverage Qualcomm’s technology to create a truly connected world. Qualcomm is 12-24 months ahead of our merchant competitors in the transition to 5G – a result of our innovation and technological advancements. We have already partnered with many companies to bring 5G to market, including Verizon, AT&T and multiple operators globally. We are the partner of choice for infrastructure vendors such as Ericsson, Nokia, Samsung and others. All OEMs and operators working to bring 5G to the market are working with Qualcomm.

Our advantage in 5G is a direct outcome of our leadership in 4G and our long-term R&D investments. Qualcomm is the only company to successfully lead in each mobile technology transition, in every case emerging as a larger and even better positioned company. 5G will be no different. Leading in 5G builds upon success and leadership in 4G, particularly 4G LTE Advanced, upon which the 5G technology is built. No other company comes close to Qualcomm on 4G LTE Advanced or on 5G.

|

“QCOM is center stage in shaping the 5G standard and is a major IP contributor and no semiconductor company is investing as much in 5G or has as much to gain as QCOM.” |

Beyond 2019: Opportunities Have Never Been Greater

Qualcomm’s leadership in 5G, coupled with our strength in connectivity, low power compute and security, has positioned us for healthy long-term growth in areas such as mobile RF front end, IoT, automotive, computing and networking. These opportunities represent a serviceable addressable market (“SAM”) of $150 billion by 2020; more than 6 times the size of Qualcomm’s SAM in 2015. We expect growth in these new areas to drive robust value creation for stockholders beyond 2019. We are demonstrating success in these areas with more than $3 billion in revenues in 2017, up 75% over the last two years.

QUALCOMM’S BOARD IS COMMITTED AND BEST QUALIFIED TO EXECUTE THE STRATEGY TO DRIVE VALUE CREATION FOR ALL QUALCOMM STOCKHOLDERS

Qualcomm’s world-class, independent and recently refreshed Board has been instrumental in the design and execution of Qualcomm’s strategy, and has a deep understanding of, and vast experience in, the global semiconductor business and relevant adjacent industries. The Board is comprised of business leaders with technology and regulatory expertise, M&A experience, investment expertise, and track records of transforming companies and creating substantial value.

The Board is committed to representing the best interests of and maximizing value for Qualcomm stockholders, and has a proven record of taking proactive, decisive action to create stockholder value and navigating difficult challenges, both regulatory and at the customer level. Over the past three fiscal years, the Board has:

- Overseen the Strategic Realignment Plan, which drove significant value creation and strategically strengthened Qualcomm

- Delivered $1.4 billion in cost reductions

- Returned over $25 billion to stockholders through dividends and share repurchases

- Resolved China licensing issue and rolled out licensing program in China (120 new licensees)

- Diversified revenues and led Qualcomm through the acquisition of CSR, the RF360 joint venture with TDK, and the pending acquisition of NXP

- Established a strategy that drove an upward stock price trajectory prior to Apple filing a lawsuit and stopping its contract manufacturers’ payment of their licensing obligations

Most importantly, Qualcomm’s existing Board understands and is well versed in Qualcomm’s complex business. This is not true for Broadcom’s inherently conflicted nominees who have minimal relevant experience and are likely to act in the best interests of Broadcom and Silver Lake. While Broadcom pursues its uncertain regulatory path for 18 months or more, Qualcomm will be executing on a plan that will ramp up value creation, including capturing the 5G opportunity and resolving licensing disputes.

Moreover, if Broadcom continues to pursue its hostile bid, the Board will be responsible (on behalf of Qualcomm stockholders) for running Qualcomm’s business to maximize its value and, if a deal is the best outcome for Qualcomm stockholders, ensuring Broadcom pays an appropriate value. Qualcomm stockholders – who would you rather have running your business, negotiating on your behalf with respect to Broadcom and managing your investment during this critical timeframe?

BROADCOM’S OPPORTUNISTIC PROPOSAL DRAMATICALLY UNDERVALUES QUALCOMM AND THERE IS SIGNIFICANT DOUBT ABOUT WHETHER IT CAN EVER BE COMPLETED

Broadcom’s $70 per share proposal dramatically undervalues Qualcomm, implying a P/E multiple of approximately 10x based on Qualcomm’s expected FY 2019 Non-GAAP EPS of $6.75 to $7.50. For context, the SOX semiconductor index currently trades at 19x and precedent transactions in the sector have averaged 22x.

The math is clear – on a near-term value basis alone Broadcom’s proposal dramatically undervalues Qualcomm, without even taking into account the substantial longer term upside from 5G. No matter how you look at it, Broadcom’s proposal is not worthy of discussion from a value perspective.

Broadcom’s Proposal Comes with Substantial Regulatory Challenges with

No Commitments to Resolution

This potential transaction would require clearance from at least a dozen antitrust regulators throughout the world, including the U.S., EU, China, Korea, Japan and others, as well as from national security agencies. Regulatory review would likely take at least 18 months to complete, if ever, and would likely require meaningful divestitures, ongoing restrictions on the combined entity’s conduct, potentially contradictory and irreconcilable demands from regulators, and the transaction could be blocked outright.

Simply put, Broadcom is asking Qualcomm stockholders to assume tremendous risk and forgo significant potential value for the sole benefit of Broadcom stockholders. Broadcom is trying to force Qualcomm stockholders to make a decision before Qualcomm’s substantial 5G and other value opportunities are realized, while the stock is temporarily disrupted by Apple’s litigation. Broadcom has compiled a board slate of nominees, a majority of whom are friends of Silver Lake, rather than truly independent nominees or nominees with large cap tech board expertise. Broadcom also has done nothing to address its proposal’s substantial regulatory risk. Why is Broadcom now launching a proxy fight to replace Qualcomm’s Board when its proposed transaction has no clear path to completion?

VOTE THE WHITE PROXY CARD TODAY AND DISCARD THE BLUE PROXY CARD IN ORDER TO BLOCK BROADCOM’S DRAMATICALLY UNDERVALUED PROPOSAL

We strongly urge you to vote to re-elect Qualcomm’s entire slate of 11 highly qualified and experienced nominees. Your vote is very important, no matter how many shares you own. Support your Board by voting the WHITE proxy card TODAY. Please follow the instructions on the enclosed WHITE proxy card to vote by Internet, telephone or sign, date and return the enclosed WHITE proxy card in the postage-paid envelope provided. Do not return any Blue proxy card you may receive from Broadcom.

VOTE the WHITE proxy card today.

Re-elect the Qualcomm Board online, by telephone, or by signing, dating and returning the WHITE proxy card in the postage-paid envelope provided.

DISCARD the Blue proxy card from Broadcom.

Voting the BLUE proxy card, even if you “withhold” on all nominees, will revoke any vote you had previously submitted on Qualcomm’s WHITE proxy card. You have every right to change your vote - only your latest-dated proxy will be counted at the 2018 Annual Meeting.

We want to thank you for your continued support and we look forward to continuing our engagement with you as we work to deliver substantial additional stockholder value in the years ahead.

The Board of Directors of Qualcomm

|

Barbara T. Alexander |

Ann M. Livermore |

Clark T. Randt, Jr. |

If you have questions, or need assistance in voting your shares, please contact:

INNISFREE M&A INCORPORATED

Stockholders May Call:

Toll-Free (877) 456-3442 (from the U.S. and Canada)

(412) 232-3651 (from other locations)

Banks and Brokers May Call Collect: (212) 750-5833

About Qualcomm

Qualcomm's technologies powered the smartphone revolution and connected billions of people. We pioneered 3G and 4G – and now we are leading the way to 5G and a new era of intelligent, connected devices. Our products are revolutionizing industries, including automotive, computing, IoT, healthcare and data center, and are allowing millions of devices to connect with each other in ways never before imagined. Qualcomm Incorporated includes our licensing business, QTL, and the vast majority of our patent portfolio. Qualcomm Technologies, Inc., a subsidiary of Qualcomm Incorporated, operates, along with its subsidiaries, all of our engineering, research and development functions, and all of our products and services businesses, including, our QCT semiconductor business. For more information, visit Qualcomm’s website, OnQ blog, Twitter and Facebook pages.

ADDITIONAL INFORMATION

Qualcomm has filed a definitive proxy statement and WHITE proxy card with the U.S. Securities and Exchange Commission (the “SEC”) in connection with its solicitation of proxies for its 2018 Annual Meeting of Stockholders (the “2018 Annual Meeting”). QUALCOMM STOCKHOLDERS ARE STRONGLY ENCOURAGED TO READ THE DEFINITIVE PROXY STATEMENT (AND ANY AMENDMENTS AND SUPPLEMENTS THERETO) AND ACCOMPANYING WHITE PROXY CARD AS THEY CONTAIN IMPORTANT INFORMATION. Stockholders may obtain the proxy statement, any amendments or supplements to the proxy statement and other documents as and when filed by Qualcomm with the SEC without charge from the SEC’s website at www.sec.gov.

CERTAIN INFORMATION REGARDING PARTICIPANTS

Qualcomm, its directors and certain of its executive officers may be deemed to be participants in connection with the solicitation of proxies from Qualcomm’s stockholders in connection with the matters to be considered at the 2018 Annual Meeting. Information regarding the identity of potential participants, and their direct or indirect interests, by security holdings or otherwise, is set forth in the proxy statement and other materials to be filed with the SEC. These documents can be obtained free of charge from the sources indicated above.

CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS

Any statements contained in this document that are not historical facts are forward-looking statements as defined in the U.S. Private Securities Litigation Reform Act of 1995. Additionally, statements regarding operating results for future years, growth in operating results and the factors contributing to future operating results; the resolution of licensing disputes and the impact and timing thereof; expected market, industry, geographic and organic growth and trends; future serviceable addressable market size and growth; anticipated contributions from and growth in new opportunities; benefits from planned cost reductions; technology and product leadership and trends; Qualcomm’s positioning to benefit from any of the above; potential benefits and upside to Qualcomm’s stockholders related to any of the above; and the regulatory process and regulatory uncertainty are forward-looking statements. Words such as “anticipate,” “believe,” “estimate,” “expect,” “forecast,” “intend,” “may,” “plan,” “project,” “predict,” “should,” “will” and similar expressions are intended to identify such forward-looking statements. These statements are based on Qualcomm’s current expectations or beliefs, and are subject to uncertainty and changes in circumstances. Actual results may differ materially from those expressed or implied by the statements herein due to changes in economic, business, competitive, technological, strategic and/or regulatory factors, and other factors affecting the operations of Qualcomm. More detailed information about these factors may be found in Qualcomm’s filings with the SEC, including those discussed in Qualcomm’s most recent Annual Report on Form 10-K and in any subsequent periodic reports on Form 10-Q and Form 8-K, each of which is on file with the SEC and available at the SEC’s website at www.sec.gov. SEC filings for Qualcomm are also available in the Investor Relations section of Qualcomm’s website at www.qualcomm.com. Qualcomm is not obligated to update these forward-looking statements to reflect events or circumstances after the date of this document. Readers are cautioned not to place undue reliance on these forward-looking statements, which speak only as of their dates.

NOTE REGARDING USE OF NON-GAAP FINANCIAL MEASURES

The Non-GAAP financial information presented herein should be considered in addition to, not as a substitute for or superior to, financial measures calculated in accordance with GAAP. In addition, “Non- GAAP” is not a term defined by GAAP, and as a result, the Company’s measure of Non-GAAP results might be different than similarly titled measures used by other companies. Reconciliations between GAAP and Non-GAAP results are presented herein.

The Company uses Non-GAAP financial information: (i) to evaluate, assess and benchmark the Company’s operating results on a consistent and comparable basis; (ii) to measure the performance and efficiency of the Company’s ongoing core operating businesses, including the QCT (Qualcomm CDMA Technologies) and QTL (Qualcomm Technology Licensing) segments; and (iii) to compare the performance and efficiency of these segments against competitors. Non-GAAP measurements used by the Company include revenues, cost of revenues, R&D expenses, SG&A expenses, other income or expenses, operating income, interest expense, net investment and other income, income or earnings before income taxes, effective tax rate, net income and diluted earnings per share. The Company is able to assess what it believes is a more meaningful and comparable set of financial performance measures for the Company and its business segments by using Non-GAAP information. In addition, the Compensation Committee of the Board of Directors uses certain Non-GAAP financial measures in establishing portions of the performance-based incentive compensation programs for our executive officers. The Company presents Non-GAAP financial information to provide greater transparency to investors with respect to its use of such information in financial and operational decision-making. This Non-GAAP financial information is also used by institutional investors and analysts in evaluating the Company’s business and assessing trends and future expectations.

Non-GAAP information used by management excludes its QSI segment and certain share-based

compensation, acquisition-related items, tax items and other items.

- QSI is excluded because the Company expects to exit its strategic investments in the foreseeable future, and the effects of fluctuations in the value of such investments and realized gains or losses are viewed by management as unrelated to the Company’s operational performance.

- Share-based compensation expense primarily relates to restricted stock units. Management believes that excluding non-cash share-based compensation from the Non-GAAP financial information allows management and investors to make additional comparisons of the operating activities of the Company’s ongoing core businesses over time and with respect to other companies.

- Certain other items are excluded because management views such items as unrelated to the operating activities of the Company’s ongoing core businesses, as follows:

- Acquisition-related items include amortization of certain intangible assets, recognition of the step-up of inventories to fair value and the related tax effects of these items, as well as any effects from restructuring the ownership of such acquired assets. Additionally, the Company excludes expenses related to the termination of contracts that limit the use of the acquired intellectual property, third-party acquisition and integration services costs and costs related to temporary debt facilities and letters of credit executed prior to the close of an acquisition. Starting with acquisitions in the second quarter of fiscal 2017, the Company excludes recognition of the step-up of property, plant and equipment from the net book value based on the original cost basis to fair value. Such charges related to acquisitions that were completed prior to the second quarter of fiscal 2017 continue to be allocated to the segments, and such amounts are not material.

- The Company excludes certain other items that management views as unrelated to the Company’s ongoing business, such as major restructuring and restructuring-related costs, goodwill and indefinite- and long-lived asset impairments and awards, settlements and/or damages arising from legal or regulatory matters.

- Certain tax items that are unrelated to the fiscal year in which they are recorded are excluded in order to provide a clearer understanding of the Company’s ongoing Non-GAAP tax rate and after tax earnings.

RECONCILIATION OF NON-GAAP FINANCIAL MEASURE